Two of China's leading optical‑module makers have reported blistering profit forecasts for 2025, a direct reflection of the global rush to scale artificial‑intelligence infrastructure and the accompanying demand for ever‑higher‑speed interconnects.

Xinyisheng (新易盛) said on January 30 that it expects 2025 net profit attributable to shareholders of ¥94–99 billion, a year‑on‑year leap of roughly 231–249 per cent, with adjusted profit excluding non‑recurring items almost identical to that figure. Zhongji Xuchuang (中际旭创) issued a similarly euphoric outlook on the same day, forecasting ¥98–118 billion in 2025 net profit, an increase of around 90–128 per cent. By contrast, Tianfu Communication (天孚通信), which reported earlier, projects a more modest but still healthy rise: adjusted net profit of ¥18.29–21.08 billion, up about 39–60 per cent.

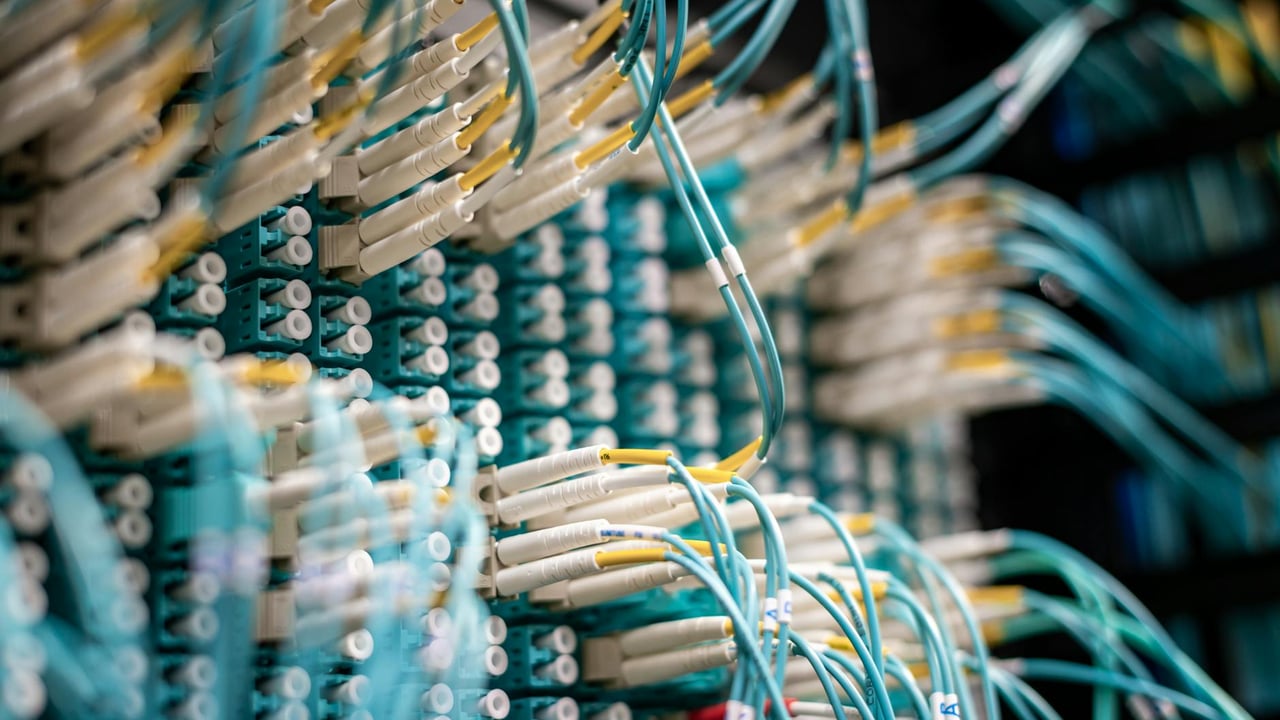

The companies point to the same structural driver: hyperscale cloud providers and large data‑centre operators are rapidly deploying AI clusters and demanding high‑bandwidth optical modules—especially 800G and above. Xinyisheng's filing highlights the firm’s strong position in high‑speed optical modules and stresses that nearly all of its profit expansion is driven by core operations rather than one‑off gains. That suggests the jump is rooted in real demand rather than accounting quirks.

Zhongji Xuchuang's announcement similarly credits its optical‑module business for most of the expansion, but its statement is notable for listing several financial offsets. The company flagged about ¥270 million of translation losses from a weaker dollar, roughly ¥113 million of provisions for slow‑moving inventory and doubtful receivables, and about ¥223 million of share‑based payment expenses that reduced headline profit. Investment income partly offset those items, adding roughly ¥296 million.

Tianfu framed its own growth as validation of sustained demand for high‑speed optical devices driven by AI and the global build‑out of data‑centre capacity. The company acknowledged macro‑related pressures, such as currency swings and elevated financing costs, but said product mix improvements and gains from intelligent manufacturing have supported margins and volumes.

These forecasts underline two trends shaping the global compute ecosystem. First, the economics of training and serving large AI models make ultra‑high‑bandwidth optics a ‘must‑have’ rather than a luxury. Vendors with the technical know‑how and manufacturing scale to produce 800G (and evolving to higher speeds) are seeing sharply elevated revenue per unit and, by extension, rapid profit growth. Second, the industry is maturing into a high‑stakes supplier market where a handful of firms capture large shares of new orders—amplifying winners' gains while leaving laggards exposed.

For investors and policymakers the headlines carry both opportunity and caution. The surge in reported profits points to robust demand that looks more structural than cyclical for now, supported by multi‑year capital programmes at cloud providers. Yet the sector faces familiar risks: foreign exchange volatility, inventory write‑downs if demand normalises, margin pressure from competition and potential downstream commoditisation, and geopolitically driven supply‑chain disruptions. Close attention to order backlogs, average selling prices and customers’ capex plans will be essential to judge whether this profitability can be sustained.

Finally, the disparity in scale is striking. Two firms are projecting near‑hundred‑billion‑yuan net profits, while a third projects less than a quarter of that. That divergence will matter for market dynamics—pricing power, investment capacity and the ability to fund R&D and vertical integration—shaping who leads the next phase of optical‑component technology.