China’s A‑share market closed the lunar Year of the Snake on a downbeat note on Feb. 14, with the three major indices sliding more than 1% after a day of intraday volatility. The Shanghai Composite fell 1.26% to 4,082.07, the Shenzhen Component dropped 1.28% to 14,100.19 and the ChiNext index lost 1.57% to 3,275.96. Turnover across Shanghai and Shenzhen was light: total daily volume came in at about CNY 1.98 trillion, under the CNY 2 trillion mark that market participants often watch as a sign of robust activity, and roughly 3,900 stocks across Shanghai, Shenzhen and Beijing ended lower.

Sector rotation characterised the session, with pockets of strength in defence equipment, cinema chains, paper, semiconductor equipment and automotive smart‑cockpit suppliers while solar equipment, minor metals, steel, ports and shipping, oil and gas services, glyphosate makers, rare‑earth permanent magnets and chemical companies lagged. The robotics theme revived in the afternoon after comments by Yushuzhihui (Yushi) founder and CEO Wang Xingxing, who told CCTV that “embodied intelligence” — AI integrated into robots and physical systems — could one day dwarf the mobile‑internet boom in scale and attention. That remark helped names such as Shuanglin (双林股份) soar more than 10%, while other automation and robotics plays pushed higher.

Printed circuit board (PCB) related stocks also rallied after copper‑foil suppliers jumped, with Tongguan Copper Foil (铜冠铜箔) rising more than 10% to a new high. The move followed an announcement by Japan’s semiconductor materials maker Resonac that it will increase prices of copper‑clad laminates (CCL), adhesive films and other PCB inputs by over 30% from March 1, a change that would directly affect PCB margins and downstream electronics costs. Domestic PCB material names such as Huibo New Materials (惠柏新材) and Jiangnan New Material (江南新材) tracked higher on the news.

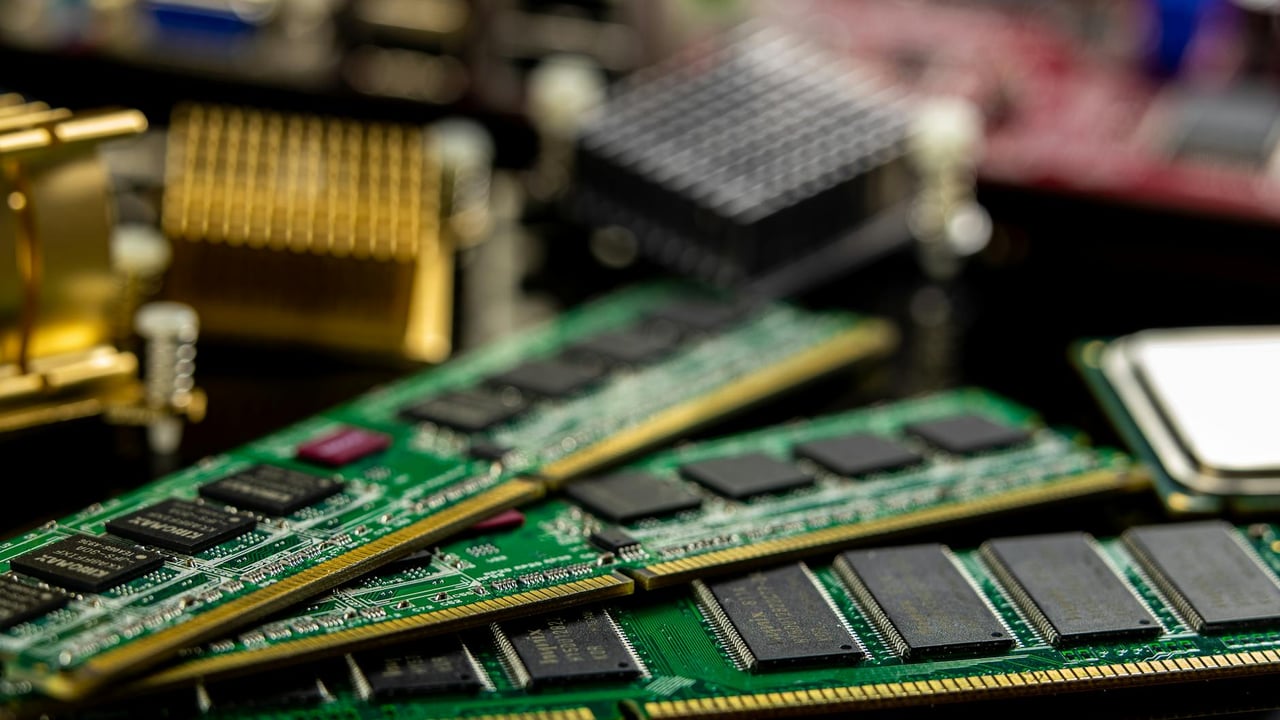

Meanwhile, memory chip stocks unexpectedly outperformed amid a sharp snapback in DRAM prices. A Counterpoint price‑tracking report cited by the market showed that memory prices rose 80–90% quarter‑on‑quarter into Q1 2026, driven principally by a rebound in general‑purpose server DRAM. That helped several storage and memory suppliers rally, with Shenzhen Technology (深科技) hitting its daily limit‑up and other chip names following suit. Conversely, the CPO (communications‑platform‑oriented) theme weakened in the afternoon, with several stocks posting outsized losses and some hitting circuit breakers.

Brokerage research notes are amplifying the narrative that structural demand will sustain equipment spending. China Galaxy Securities flagged strong growth expectations for the 2026 semiconductor equipment market, pointing to persistent AI compute demand, an upturn in the memory cycle and deeper adoption of advanced packaging; Taiwan’s TSMC is forecast to boost capital expenditure to USD 52–56 billion in 2026, underscoring the scale of investment in chips. CITIC Securities highlighted an accelerating policy push on data security in China, arguing that tighter rules and enforcement will sustain demand for cybersecurity products and services and create durable winners among vendors with broad product suites and enterprise footprints.

The session is a reminder of two concurrent trends shaping China’s markets: a speculative, theme‑driven rotation into technology and defence ideas on the one hand, and an underlying liquidity caution around major calendar events on the other. The recent surge in memory prices and the prospect of sustained equipment spending are constructive for the semiconductor supply chain, but several cross‑currents — material price inflation, policy‑driven demand for domestic cybersecurity solutions, and uneven market breadth — mean gains may be concentrated and volatile rather than broad‑based.