SpaceX has long enjoyed a reputation for engineering miracles, but its latest financial disclosure suggests the laws of economics are proving harder to defy than gravity. Despite reaching a staggering $18.5 billion in annual revenue, the aerospace giant reportedly closed the year with a $5 billion net loss. This fiscal crater is not the result of failed launches or satellite failures, but rather a strategic entanglement with Elon Musk’s AI venture, xAI.

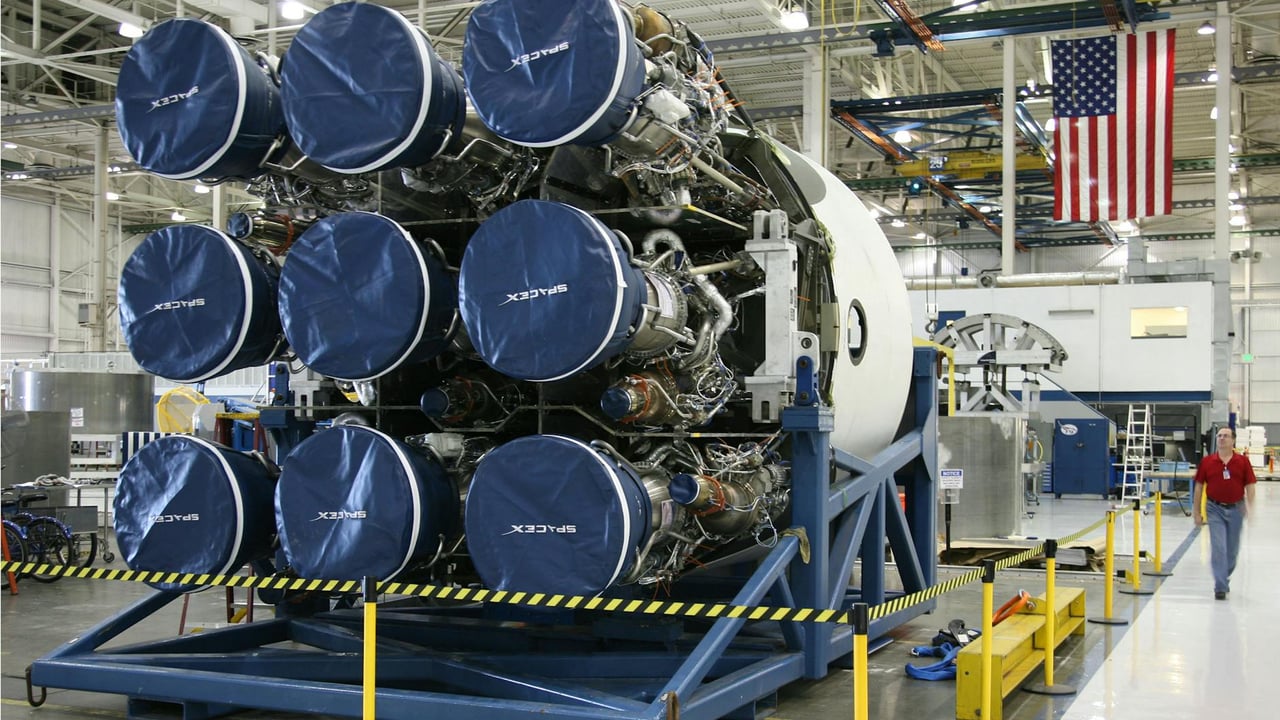

The core fundamentals of SpaceX’s aerospace business remain remarkably robust. Propelled by the Falcon 9’s dominance in the launch market and Starlink’s growing subscriber base of over 9 million, the traditional space segments generated nearly $8 billion in EBITDA. However, this operational health has been compromised by the aggressive acquisition and integration of xAI, which forced SpaceX to absorb massive expenditures for data centers and specialized silicon.

With xAI’s burn rate reaching an estimated $1 billion per month, the financial burden has outpaced the organic cash flow of the satellite and rocket divisions. This disparity explains the sudden urgency behind SpaceX’s upcoming IPO roadshow, where the company aims to raise $75 billion from public markets. The proposed $2 trillion valuation, however, is being met with significant skepticism from Wall Street, where analysts point to a price-to-earnings ratio that appears decoupled from traditional fundamentals.

Internal governance is also under strain as the company maneuvers toward its June listing. The departure of high-ranking financial and founding members, including former xAI CFO Anthony Armstrong, signals friction during the integration process. To mitigate investor concerns and stabilize cash flow, Musk has reportedly pivoted the company’s immediate narrative away from the long-term colonization of Mars toward more lucrative, government-funded lunar contracts under NASA’s Artemis program.

Ultimately, the SpaceX IPO represents a high-stakes bet on Musk’s vision of a 'sovereign AI' infrastructure—a world where orbital constellations provide the massive compute power required for the next generation of intelligence. For potential investors, the decision rests on whether they view the company as a stable aerospace monopoly or a speculative vehicle for Musk’s broader technological ambitions. As the April 20 roadshow approaches, the market’s appetite for this space-AI nexus will face its most rigorous test yet.