Zhongji Innolight, the world’s leading optical module manufacturer, briefly joined the ranks of China’s trillion-yuan market-cap elites this April. The company’s valuation surge to 1 trillion RMB marks it as only the second computing hardware firm in the A-share market, after Foxconn Industrial Internet, to cross this psychological threshold. This milestone is a direct consequence of the global AI arms race, which has turned once-obscure hardware components into high-value strategic assets.

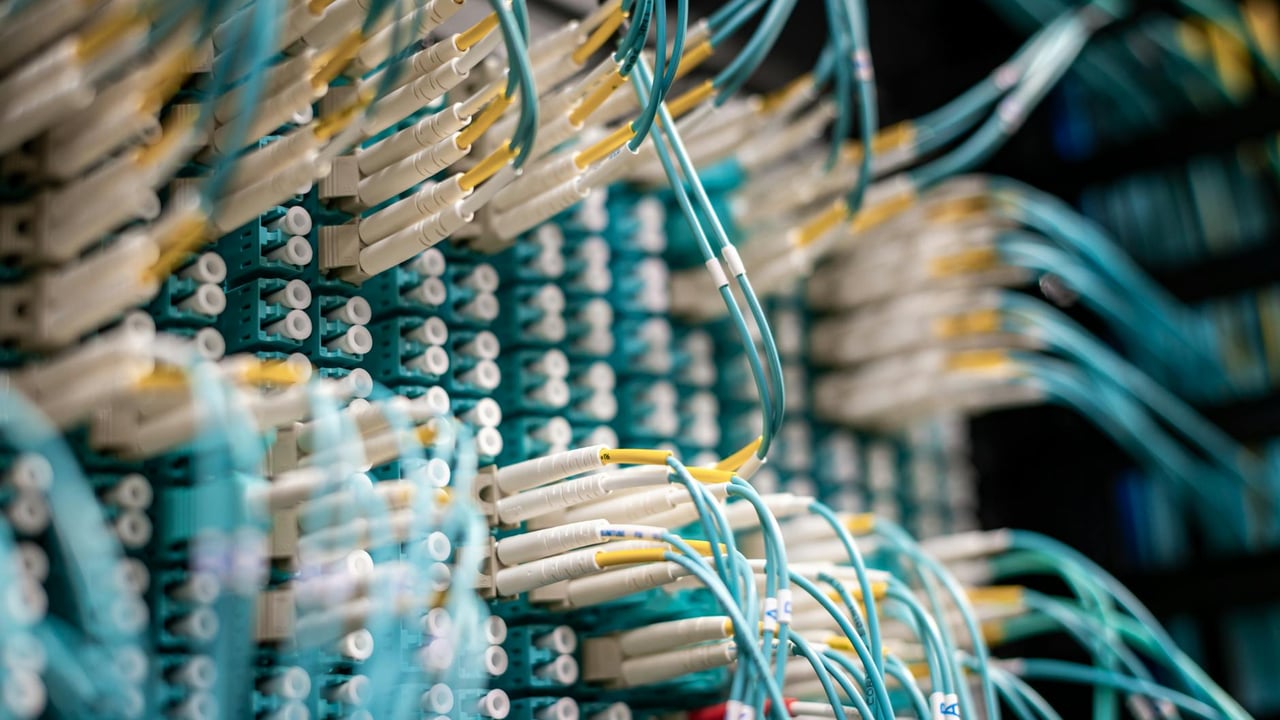

At the heart of this financial explosion is the 75-year-old founder, Wang Weixiu, who has seen his family wealth skyrocket to 105 billion RMB. The company’s first-quarter performance for 2026 justified much of the investor enthusiasm, with revenues jumping nearly 200% and net profits exceeding 5.7 billion RMB—already surpassing the firm’s total earnings for the entirety of 2024. This growth is fueled by the relentless demand from cloud service providers for 800G and 1.6T optical modules, the essential conduits for high-speed AI data processing.

However, the euphoria is tempered by significant operational strain. Zhongji Innolight’s prepayments to suppliers have ballooned tenfold in a single quarter, rising from 134 million RMB to nearly 1.5 billion RMB. This surge reflects a desperate scramble to secure critical raw materials like indium phosphide substrates and electro-absorption modulated laser (EML) chips, which remain under the tight control of a few overseas monopolistic suppliers. The company is essentially paying a premium to lock in capacity amidst a global shortage that threatens to throttle delivery schedules.

Beyond supply chain bottlenecks, the firm faces a precarious geopolitical reality. Over 90% of its revenue is generated in overseas markets, primarily North America, leaving it vulnerable to the shifting winds of US-China trade policy. The company itself has warned that any escalation in trade sanctions could not only cripple its ability to source core components but also shut it out of its most lucrative markets. With a customer concentration where five entities account for over 75% of sales, the loss of a single major client would be catastrophic.

Market observers remain divided on whether this trillion-yuan valuation is sustainable or a symptom of an AI-induced bubble. While the company dominates the high-speed 1.6T module market, critics point out that its core value remains in sophisticated assembly rather than fundamental semiconductor innovation. As competitors like Luxshare Precision begin to eye the sector and technology cycles move toward 3.2T modules, the current fat margins enjoyed by the 'Yi-Zhong-Tian' trio may face the same commodity-style erosion seen in the renewable energy sector.