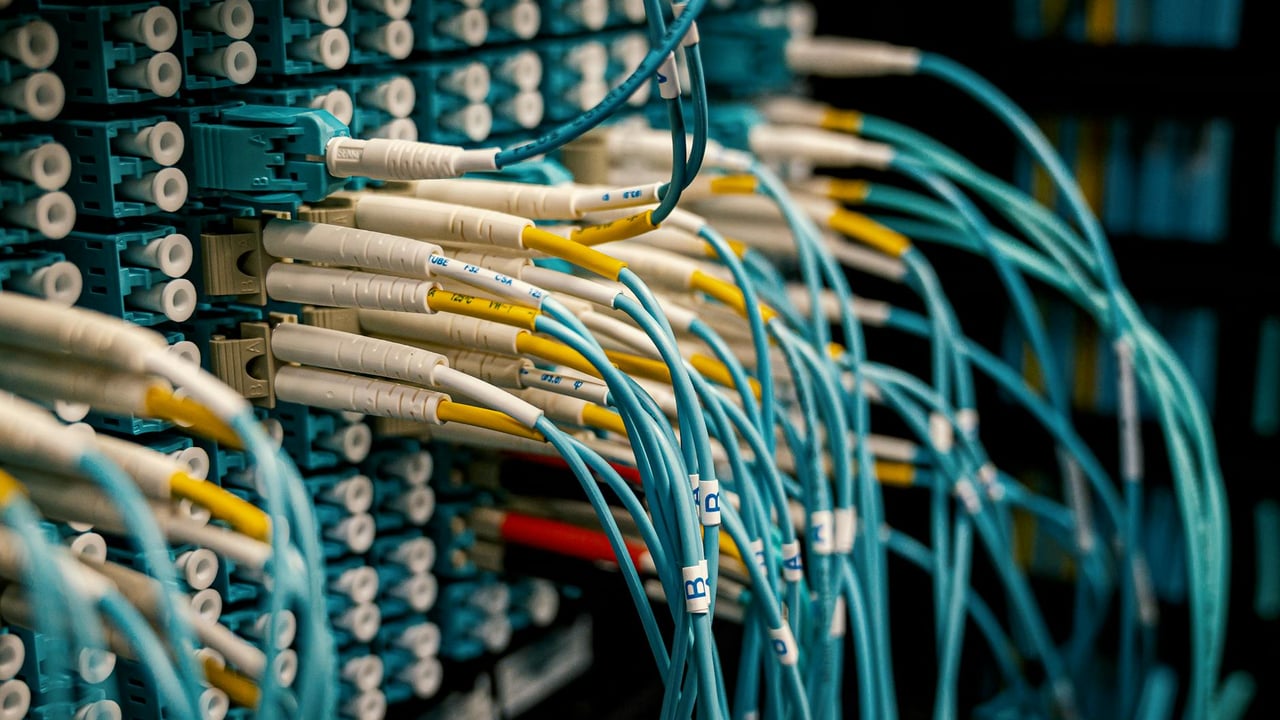

The global race for artificial intelligence is often framed as a battle over high-end silicon, yet a more visceral bottleneck is emerging in the physical layers of the internet. In the first quarter of 2024, Chinese manufacturers of specialty optical fibers and optical modules—the literal glass and light of the digital age—reported an unprecedented surge in demand. Prices for specialty optical fibers have skyrocketed tenfold within a single year, yet even at these premiums, supply remains agonizingly tight. For many Chinese firms, the order books are now filled through 2028, reflecting a desperate global scramble to build the infrastructure required for the generative AI era.

This frenzy is driven by the explosive growth of massive data centers and the exponential demand for bandwidth. As AI models grow larger and more complex, the speed at which data travels between servers has become as critical as the processing power of the chips themselves. In Wuhan, a major hub for China’s telecommunications industry, firms are now mass-producing 1.6T optical modules. These devices, capable of transmitting nearly 200 gigabytes of data per second, are retailing for approximately $1,000 a unit and have become the most sought-after hardware for international hyperscalers.

China’s grip on this sector is increasingly formidable. The country now controls roughly 70% of the global optical module market and 60% of the world’s optical fiber supply. This is no longer a story of low-end commodity manufacturing; Chinese firms are now leading in high-frontier technologies like hollow-core fibers and super-interconnect modules. The current supply-demand imbalance is so severe that customers are reportedly paying upfront deposits simply to lock in production capacity years in advance, a level of leverage rarely seen in the telecommunications hardware space.

This shift places Chinese manufacturers at the center of the global AI supply chain. While Western governments have focused on restricting China’s access to advanced GPUs, the infrastructure required to connect those GPUs is increasingly a Chinese specialty. As global computing power centers continue to proliferate, the reliance on Chinese optical technology suggests that the decoupling of the high-tech supply chain may be far more difficult in the physical layer than it is in the logic layer.