In the sprawling landscape of China's semiconductor and hardware sectors, few success stories are as visceral as the rise of InnoLight Technology. As the company's market capitalization surged past the one-trillion-yuan threshold, it did more than just signal a victory for Chinese manufacturing; it fundamentally altered the financial destinies of its workforce. With an estimated 2,000 employees and executives holding shares, the average value per recipient has ballooned to roughly 31 million yuan, creating a localized wealth effect rarely seen outside of Silicon Valley's titan startups.

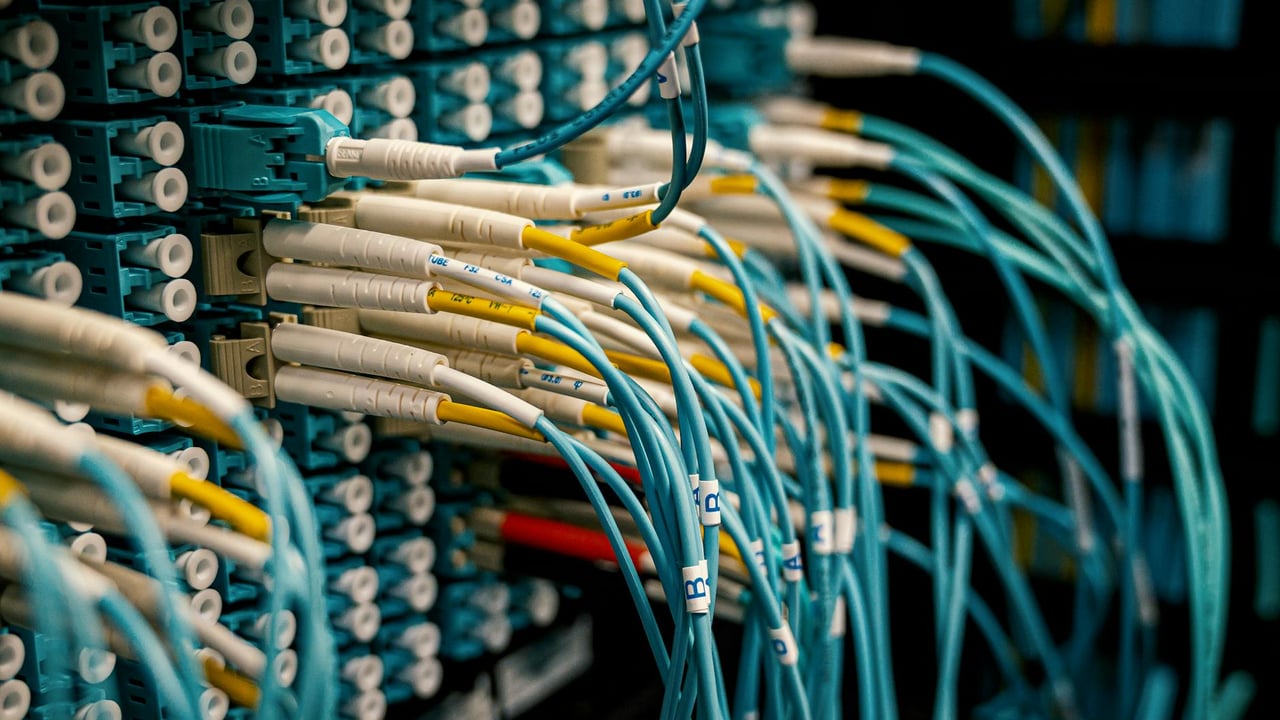

This stratospheric growth is the direct result of the global arms race for Artificial Intelligence. InnoLight has positioned itself as the indispensable plumbing of the AI era, specializing in the high-speed optical transceivers required to move data across the massive GPU clusters that train Large Language Models. As demand for 800G and 1.6T modules skyrocketed, InnoLight’s stock became a primary beneficiary of the capital flow into AI compute infrastructure, outperforming even the most optimistic market projections from previous years.

The company’s financial trajectory reflects a pivot from a domestic supplier to a global powerhouse. Since acquiring Suzhou InnoLight in 2017, the firm has seen its revenue grow sixfold while net profits have surged by a factor of 17. By 2026, the company's Q1 growth figures exceeded 190%, driven largely by its dominance in overseas markets. Remarkably, over 90% of InnoLight's revenue is now derived from international clients, primarily hyper-scalers in North America and Europe who depend on the company's manufacturing scale and technical precision.

However, this rapid ascent brings its own set of complexities. While thousands of employees celebrate their newfound paper wealth, the company is also seeing significant divestment from its upper echelons. Several top executives and institutional shareholders have begun trimming their positions as the stock hits historic highs. This tension between long-term growth and immediate liquidity for insiders is a common feature of the 'trillion-yuan club,' yet it raises questions about the sustainability of such valuations in a sector defined by rapid technological obsolescence and shifting geopolitical sands.