In the hyper-competitive landscape of Chinese technology, the physical infrastructure of the artificial intelligence revolution has become a modern-day gold mine. Zhongji Innolight, a leading manufacturer of optical transceivers, recently saw its market capitalization breach the one trillion yuan milestone, with its share price soaring past the 1,000 yuan mark. This astronomical growth has translated into a life-changing windfall for its workforce, as the company recently cleared the path for 803 employees to vest equity worth a staggering 1.7 billion yuan.

This phenomenon is not isolated to China’s borders; it mirrors a broader regional trend where the 'AI wind' is redefining social and economic hierarchies. In South Korea, employees of memory giant SK Hynix have become the most sought-after bachelors in the matchmaking market due to projected record bonuses. At Innolight, the scale of wealth distribution is even more concentrated, with a select group of 99 senior managers and core technicians recently splitting an equity pool valued at 2.6 billion yuan, averaging over 26 million yuan per person.

The company’s financial trajectory provides the bedrock for this generosity. In 2025, Innolight reported record-breaking revenues of 38.2 billion yuan and a net profit of 10.8 billion yuan, figures that reflect the global scramble for high-speed data transmission in AI clusters. This performance has triggered a generational shift in China’s domestic investment scene, where younger fund managers are aggressively ditching 'old economy' staples like Kweichow Moutai in favor of high-growth AI hardware plays.

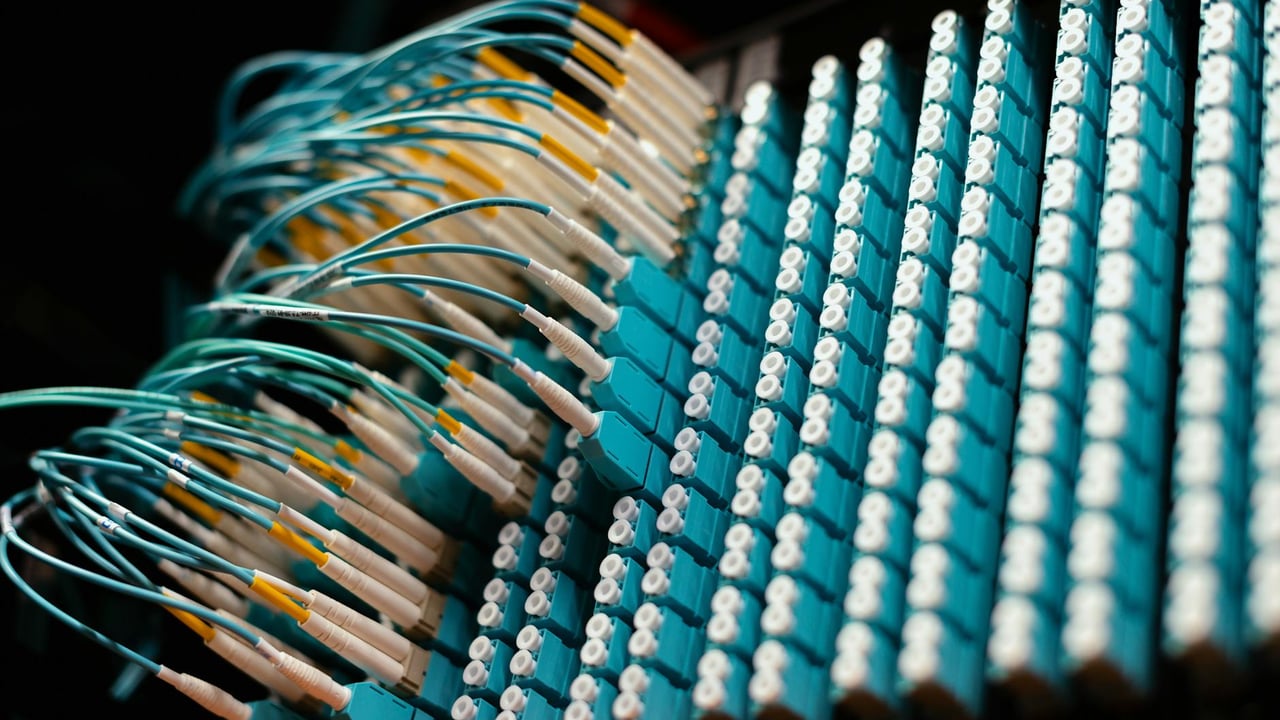

Mainland China currently controls over 60% of the global optical module market, and Innolight sits at the apex of this hierarchy. As data centers demand higher bandwidth and lower latency, the company has successfully capitalized on the transition to 800G and 1.6T modules. However, the sheer perfection of its recent earnings report has narrowed the margin for error, leaving investors increasingly sensitive to risks regarding exchange rate fluctuations and client concentration among global cloud giants.

The most significant long-term threat remains the potential shift in technological paradigms. The industry is currently eyeing Co-Packaged Optics (CPO) and silicon photonics as the next frontier for reducing power consumption in AI training. If CPO gains mass-market adoption, the traditional pluggable module market where Innolight dominates could be disrupted. The company is currently racing to secure its position in these emerging technologies to ensure that its current 'golden ticket' status is not merely a fleeting moment in the AI cycle.