As the global artificial intelligence boom drives an insatiable hunger for computing power, the hardware infrastructure behind the scenes is entering a rare 'super cycle.' At the 21st China International Optoelectronic Exposition in Wuhan, the industry’s attention shifted from the current mass-market 800G modules toward the next frontier of data transmission. Leading Chinese firms are now showcasing 12.8T and 6.4T solutions, signaling a rapid acceleration in the R&D cycle for the 'data blood vessels' of AI clusters.

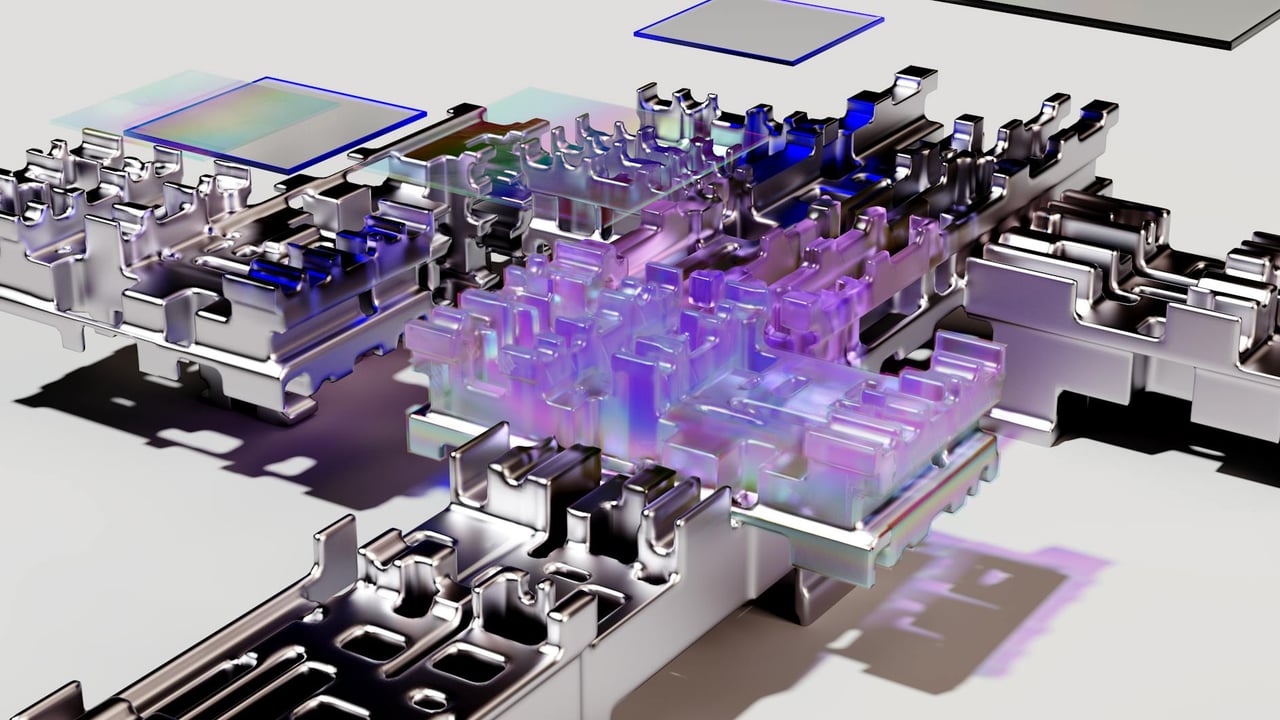

While 1.6T modules are only just beginning to see volume production, the industry is already fragmenting into a multi-track technological race. The traditional debate between pluggable optics and co-packaged optics (CPO) has evolved into a period of parallel evolution where Near-Packaged Optics (NPO) and Linear-drive Pluggable Optics (LPO) vie for dominance. This technical diversification is driven by the specific, often customized, needs of major cloud service providers who are prioritizing power efficiency and extreme density over standardized solutions.

Huagong Tech recently debuted the world’s fastest 12.8T XPO module, while Accelink Technologies unveiled 6.4T silicon photonics solutions designed specifically for AI compute clusters. These advancements highlight a broader shift toward silicon photonics, which analysts expect to capture nearly 50% of the 800G market by 2025. This transition is not just about speed; it is a strategic move to lower costs and energy consumption as interconnect distances in data centers expand from hundreds of meters to kilometers.

The financial results of these industry leaders reflect this hardware gold rush, with Zhongji Innolight reporting a staggering 262% increase in net profit for the first quarter of 2024. This surge is echoed across the supply chain, where even the raw materials for specialized AI fibers have seen price spikes of over 100% year-on-year. As cloud giants like Tencent deploy millions of silicon photonics chips, the bottleneck is shifting from design capacity to the manufacturing and simulation tools required for high-level integration.