The global race for artificial intelligence supremacy has long been framed as a battle over algorithms and high-end GPUs. However, a quieter but equally significant shift is occurring in the commodities market. Traditional industrial materials—copper, tin, indium, and gallium—are being rebranded as 'computing metals' as their market dynamics shift from being driven by legacy manufacturing to being dictated by the insatiable infrastructure demands of AI data centers.

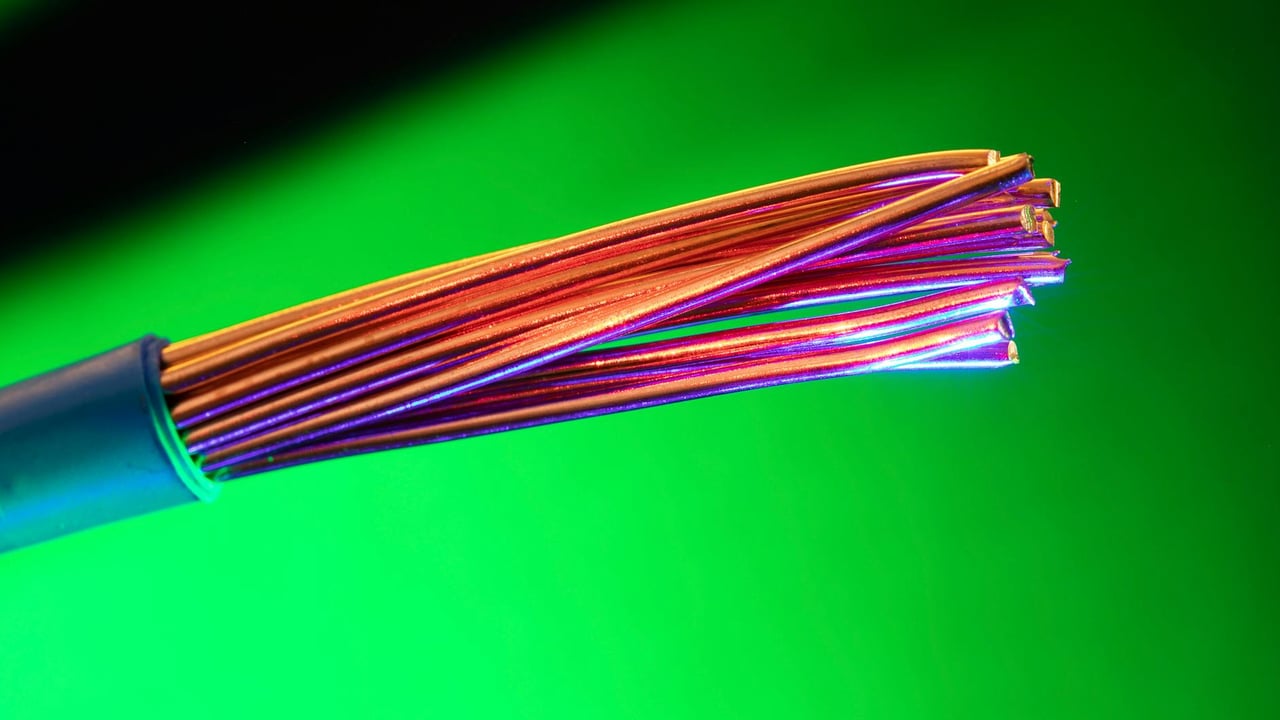

For decades, copper and tin were the unglamorous workhorses of the old economy, used in plumbing, power grids, and basic consumer electronics. Today, they are the 'circulatory system' and 'glue' of the digital age. A high-end AI server requires up to four times more copper than a standard desktop computer, while the advanced packaging of HBM (High Bandwidth Memory) and Chiplets has increased the density of tin solder points from hundreds to millions per chip.

This surge in demand is colliding with a supply side that is fundamentally inflexible. Copper mines typically require a decade-long development cycle, and rare companion metals like gallium and germanium are byproduct-dependent, meaning production cannot simply be switched on to meet a sudden spike in demand. In the current market, tin prices have recently hit three-month highs, and analysts suggest that the pricing logic has permanently shifted toward AI-driven increments rather than cyclical industrial demand.

Geopolitical friction is further complicating the supply-demand imbalance. New trade barriers, including substantial U.S. tariffs on imported copper and its derivatives slated for 2025 and 2026, are fragmenting global supply chains. As nations prioritize 'national security' in the semiconductor sector, the flow of these critical metals is becoming increasingly restricted, creating a bifurcated market where prices are prone to sudden, volatile escalations based on policy shifts rather than just consumption.

Despite the bullish long-term outlook, market participants are being warned of potential volatility. While AI infrastructure provides a high floor for demand, these metals remain sensitive to broader macroeconomic forces, including Federal Reserve interest rate policies and the pace of global AI capital expenditures. If the current wave of data center construction faces a temporary cooling or if liquidity tightens, the 'AI premium' currently baked into metal prices could face a sharp, albeit likely temporary, correction.