China’s A-share market concluded the first half of 2026 with a performance that highlights a deepening structural shift within the world’s second-largest economy. While major indices like the ChiNext surged by over 35%, a closer look reveals a highly concentrated rally where only 31% of listed companies actually delivered positive returns. This divergence underscores a "K-shaped" recovery in the capital markets, where technological self-reliance is handsomely rewarded while traditional consumer sectors languish.

The electronics sector has emerged as the undisputed engine of growth, skyrocketing nearly 76% in just six months. Leading this charge is PERIC Special Gases, which recorded a staggering 766% gain. As a dominant global supplier of tungsten hexafluoride, the company has capitalized on its critical role in the semiconductor supply chain, serving giants like TSMC and Samsung. This performance illustrates how domestic substitution in high-end electronic materials has become the primary narrative for Chinese investors seeking alpha.

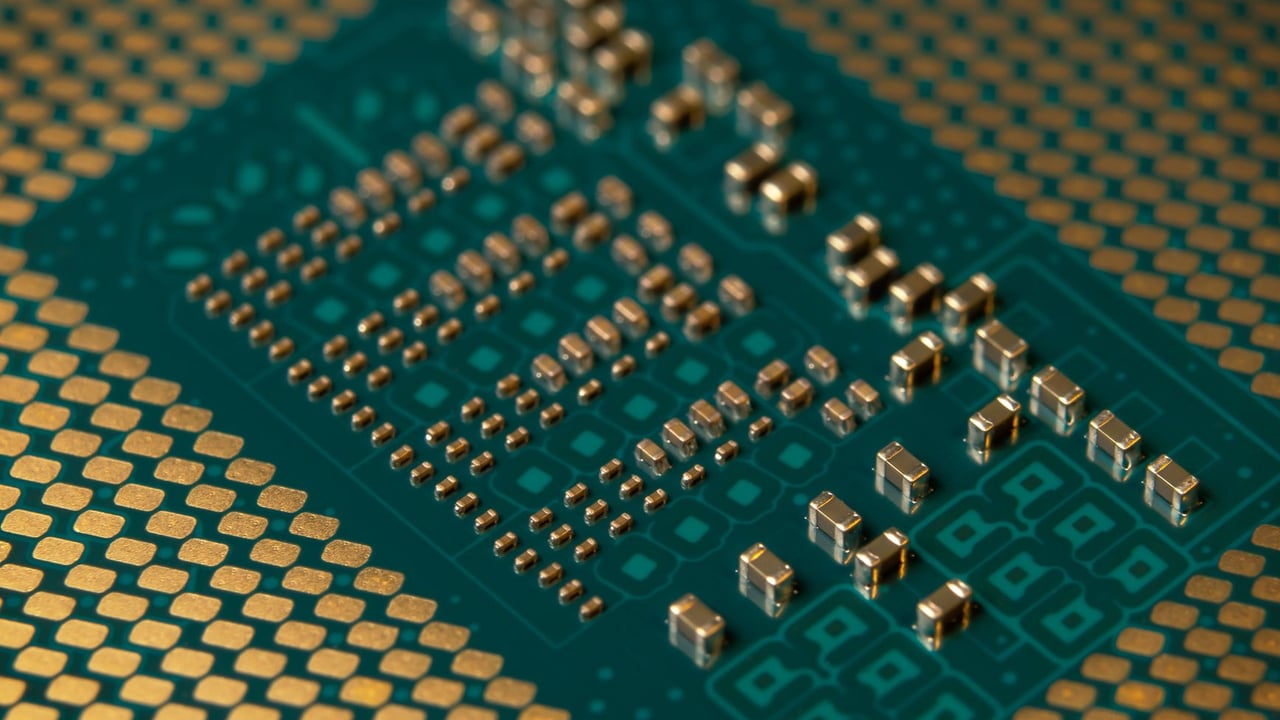

Beyond semiconductors, the artificial intelligence boom is fueling a massive re-rating of the hardware supply chain. Companies specializing in printed circuit board (PCB) materials, such as Honghe Tech and Jin’an Guoji, saw their share prices increase sixfold. These firms are benefiting from a virtuous cycle of soaring demand for AI computing power and rising upstream material costs, allowing them to exert significant pricing power in a tightening global market.

Simultaneously, the era of speculative trading in "junk stocks" appears to be coming to a definitive end. The market's worst performers in 2026 were almost exclusively composed of delisted firms and those under "Special Treatment" (ST) status, many losing over 90% of their value. This reflects a maturation of the regulatory environment, where the authorities are successfully steering capital away from chronic underperformers and toward companies with genuine industrial utility.

However, the tech-heavy rally masks persistent weakness in the broader domestic economy. While industrial and tech sectors thrived, consumer-facing industries like food and beverage, retail, and beauty products all saw declines exceeding 20%. This stark contrast suggests that while China’s "New Quality Productive Forces" are gaining momentum, the transition away from a property-led and consumption-driven growth model remains a painful and uneven process for the average investor.