Jinfu Technology, the Shenzhen-listed manufacturer long dominant in China’s beverage packaging market, is attempting a radical transformation as its core business faces significant headwinds. In its 2025 annual report, the company—often dubbed the 'Bottle Cap King' for its massive production scale—revealed a double-digit decline in both revenue and profit. Total revenue fell 14.8% to 760 million yuan, while net profit attributable to shareholders plummeted by 28.56% to approximately 101 million yuan.

Management attributed this downturn to fluctuating downstream demand and the short-term financial burden of new production bases, which incurred heavy depreciation and relocation costs. Despite a surprising surge in North China revenues, the company’s traditional strongholds in Southern and Eastern China saw marked retrenchment. This erosion of margins in the low-tech packaging sector has forced the company to look toward high-growth technology sectors to salvage its valuation.

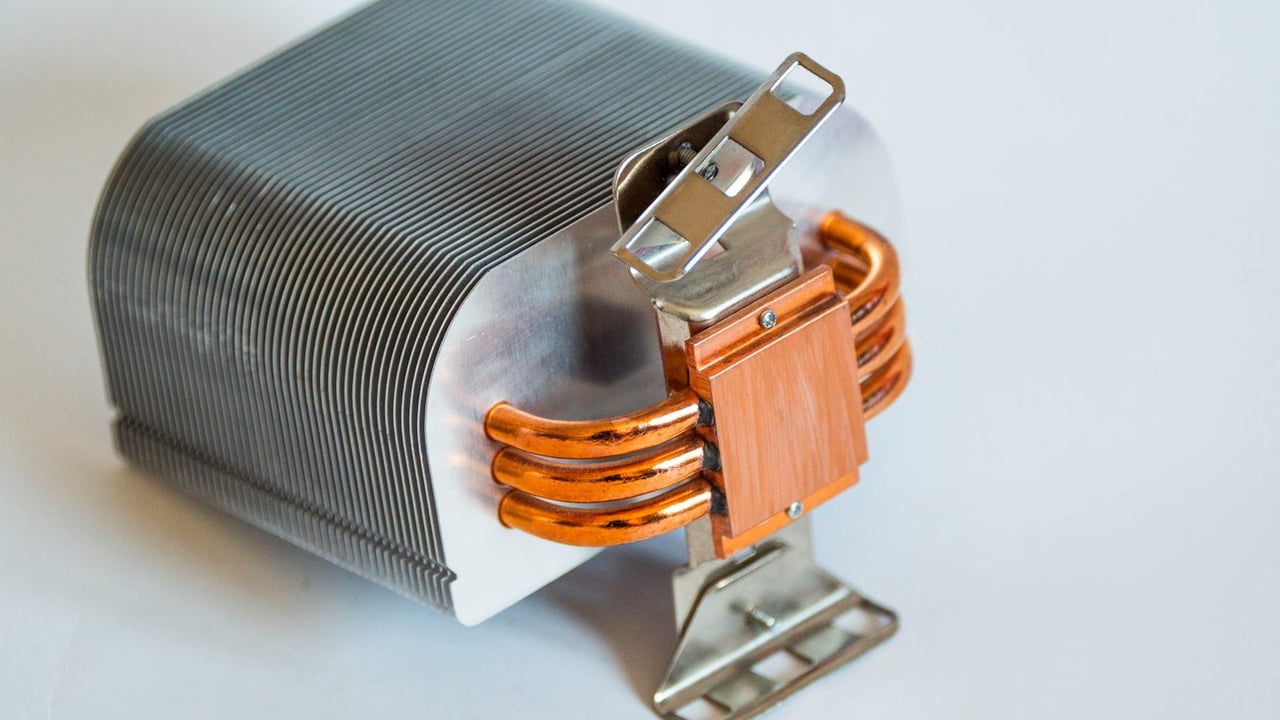

To facilitate this pivot, Jinfu Technology has announced a 571 million yuan (US$79 million) acquisition to secure 51% stakes in Zhuohui Metal and Lianyire Thermoelectric. This high-premium deal marks the company’s formal entry into the liquid cooling and thermal management sector. By diversifying into heat dissipation, Jinfu is moving from the world of soda bottles to the high-stakes infrastructure of data centers and AI computing, where efficient cooling is becoming a critical bottleneck.

The acquisition comes with rigorous strings attached, including a combined performance guarantee of at least 110 million yuan in net profit for the target companies in 2026. Jinfu has designated 2026 as the inaugural year of its 'dual-wheel drive' strategy, intending to run its packaging and thermal management divisions in tandem. However, the steep premium paid for these assets suggests a level of desperation to rebrand as a high-tech player amidst a cooling traditional economy.